The Q2 2026 global smartphone market is undergoing a massive restructuring. Consequently, a severe memory chip price surge is driving this upheaval. A recent report reveals the depths of this crisis. Specifically, the Omdia smartphone market analysis shows a 4% year-over-year decline in global shipments. Ultimately, the global memory crisis has significantly increased component costs across the board.

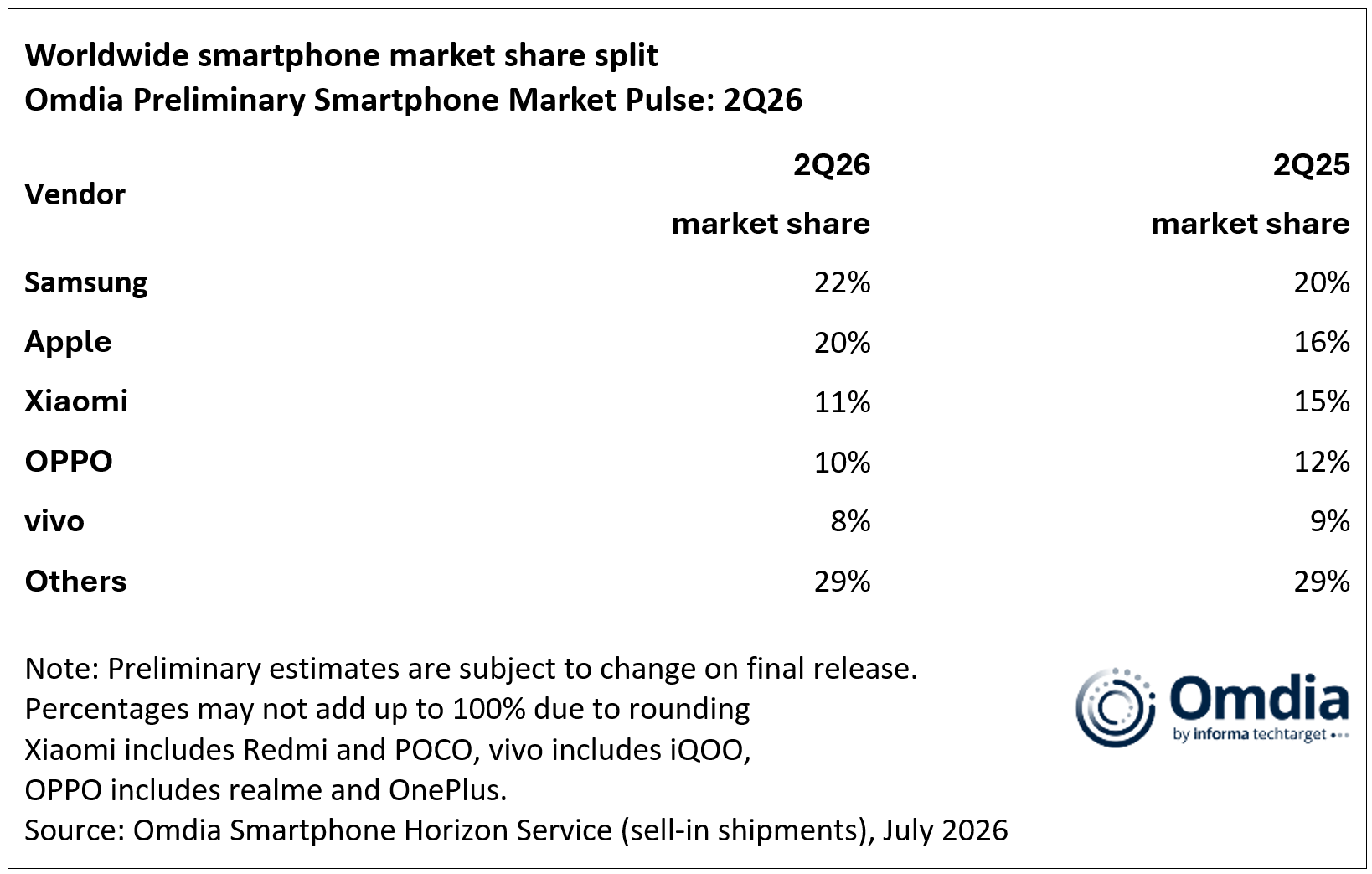

However, Apple emerged as the unexpected victor in this turbulent environment. While Android manufacturers aggressively raised prices, Apple leveraged its powerful supply chain to maintain stable pricing. Therefore, Apple captured an impressive 20% market share during a traditionally slow sales season. Indeed, this achievement marks a historical high for the company during this specific period.

The Memory Crisis Devastates the Budget Sector

A historically unprecedented spike in memory and storage chip prices is the primary culprit behind escalating component costs. For instance, DRAM prices soared by over 50% year-over-year in Q1 2026. Furthermore, NAND flash memory prices skyrocketed by an astonishing 90% during the same timeframe.

Consequently, this crisis has decimated the budget and mid-range smartphone sectors. Specifically, this impacts devices priced around $400 or lower. Some manufacturers now face memory procurement costs four to five times higher than last year. Thus, memory and storage now account for over 60% of the Bill of Materials (BOM) for entry-level devices.

Faced with severe financial losses, Android brands initiated price adjustments starting in March. Chinese brands generally increased mid-range phone prices by 300 to 1000 RMB. Naturally, this sudden spike deterred price-sensitive consumers. As a result, brands like Xiaomi, OPPO, and vivo experienced collective declines in Q2 market share.

Apple’s Supply Chain Strength and Samsung’s Resilience

In stark contrast to the Android camp, Apple’s stable pricing strategy created a unique “reverse cost-effectiveness” phenomenon. Generally, the second quarter is Apple’s weakest sales period. Typically, the company relies on older models to sustain momentum.

However, the iPhone 17 series maintained stable pricing. Moreover, Apple utilized its formidable semiconductor supply chain bargaining power effectively. Consequently, this stability triggered a robust replacement cycle. Apple’s Q2 market share surged to 20%, representing a remarkable 4% year-over-year increase.

Meanwhile, Samsung secured its position as the world’s leading smartphone manufacturer. The company achieved a 22% market share, reflecting a 2% year-over-year growth. Samsung successfully leveraged strong market demand and its incredibly robust internal semiconductor supply chain.

Q2 2026 Global Smartphone Market Share Breakdown

Unfortunately, industry analysts predict that global memory prices will not decrease until late 2027 at the earliest. Furthermore, prices are highly unlikely to return to their pre-2025 lows.

The Looming Price Storm for iPhone 18 Pro

Although the iPhone 17 series avoided the current pricing storm, future models face significant risks. Apple already increased prices across its Mac and iPad lines in late June. This adjustment indicates that supply chain cost pressures are nearing critical thresholds.

Industry experts anticipate a massive, unavoidable price hike for the upcoming iPhone 18 Pro series. Rising memory and flash storage costs alone could increase the starting price by approximately $270. Additionally, the new 2nm A20 Pro chip will add substantial foundry costs. Consequently, the starting price of the iPhone 18 Pro series might easily exceed historic boundaries.

Support Our Threat Intelligence

If you find our technology report and cybersecurity news helpful, consider supporting our work.